A customer once told us he'd spent 45 minutes at a rental desk trying to understand the difference between CDW, Super CDW, Theft Protection, and Full Coverage Waiver. The agent kept using terms like "deductible," "excess," and "irreducible deposit" without actually explaining what they meant. He walked away paying double his advertised rate and still wasn't entirely sure what he'd bought.

Insurance is where car rental companies in Morocco make their real money. That advertised 30-euro daily rate becomes 60 euros after the desk agent finishes their upsell pitch. We're going to break down exactly how rental insurance works at Agadir airport, what you actually need, and how to avoid paying for coverage you don't require.

Quick Takeaways

- Basic CDW and Theft Protection are mandatory in Morocco but include high deductibles (10,000-36,000 MAD)

- The "deductible" or "excess" is your maximum financial responsibility if something goes wrong, typically held as a deposit on your credit card

- Super CDW eliminates most of the deductible but costs 15-25 euros extra per day at traditional rental desks

- Common exclusions (tires, undercarriage, interior damage, keys) remain your responsibility even with full coverage

- Including comprehensive insurance in the base rate (our model) saves you 100-175 euros per week compared to buying it as an add-on

The Mandatory Baseline: CDW and Theft Protection

Moroccan law requires all vehicles on the road to carry insurance. When you rent from any company at Agadir airport, your contract automatically includes two core coverages: Collision Damage Waiver (CDW) and Theft Protection (TP).

Here's what travelers misunderstand about CDW. It's not actually insurance in the traditional sense, it's a waiver. The rental company agrees to waive most of their right to charge you for vehicle damage or theft. "Most" is the operative word, because there's a catch called the deductible (also called excess or franchise).

The deductible is the amount you're still responsible for even with basic CDW coverage. At Agadir airport, these deductibles typically run:

- Economy cars: 10,000-14,000 MAD (roughly 900-1,300 euros)

- Mid-size/family cars: 15,000-25,000 MAD (roughly 1,400-2,300 euros)

- SUVs and premium vehicles: 20,000-36,000 MAD (roughly 1,900-3,300 euros)

That deductible gets held on your credit card as a deposit when you pick up the car. If you return the vehicle undamaged, the hold releases in 7-14 days. If there's damage, the rental company charges whatever repair costs up to the deductible maximum.

What Super CDW Actually Does

Super CDW (also called Full CDW, Zero Excess, or Total Waiver) reduces or eliminates that deductible. Instead of being liable for up to 1,300 euros in damage, you might pay nothing or just a small "irreducible" amount (usually 200-500 MAD).

International brands at Agadir airport typically charge 15-25 euros per day for Super CDW as an optional add-on. For a week-long rental, that's 105-175 euros on top of your base rate. Some travelers gladly pay this for peace of mind. Others gamble that they won't have any incidents and skip it to save money.

The problem with buying Super CDW as an add-on is that you don't always know the true cost until pickup. The advertised rate online excludes it, then you're standing at the desk after a long flight deciding whether to spend an extra 150 euros. That's when people make expensive decisions under pressure.

The Exclusions Nobody Explains Clearly

Even with full Super CDW coverage, certain damages remain your financial responsibility. These exclusions are buried in rental contracts but they're critically important:

Tire and wheel damage from hitting potholes or curbs. Morocco has excellent highways but also plenty of rough secondary roads. Tire replacements run 100-200 euros depending on the vehicle.

Undercarriage and chassis damage from scraping speed bumps, rocks, or off-road driving. This is particularly relevant if you're heading to rural areas or mountain routes.

Interior damage including stains, burns, or excessive dirt. The definition of "excessive" is subjective and varies by company.

Lost or stolen keys, which can cost 200-400 euros because modern car keys include electronic chips that require reprogramming.

Windshield and glass damage is sometimes covered, sometimes not, depending on the specific policy and whether it was caused by negligence.

Damage from unauthorized drivers. If someone not listed on your contract drives the vehicle and causes an accident, you're fully liable regardless of insurance coverage.

Rental companies don't highlight these exclusions during the upsell conversation. They focus on selling you Super CDW without mentioning what it doesn't cover.

Third-Party Insurance: An Alternative Approach

Some travelers buy annual excess reimbursement insurance from third-party providers (companies like Insurance4CarHire or iCarhireinsurance). These policies cost 40-60 euros annually and cover deductibles across multiple rentals worldwide.

The catch is that this is "post-loss" insurance. You still pay the deductible to the rental company if damage occurs, then file a claim afterward to get reimbursed. The rental company will still hold the full deposit on your credit card at pickup because they don't recognize third-party coverage.

This option works fine if you rent cars frequently and don't mind the claims process. But for a single Morocco trip, it doesn't solve the deposit hold problem or the stress of potentially fronting 1,000+ euros for damage costs.

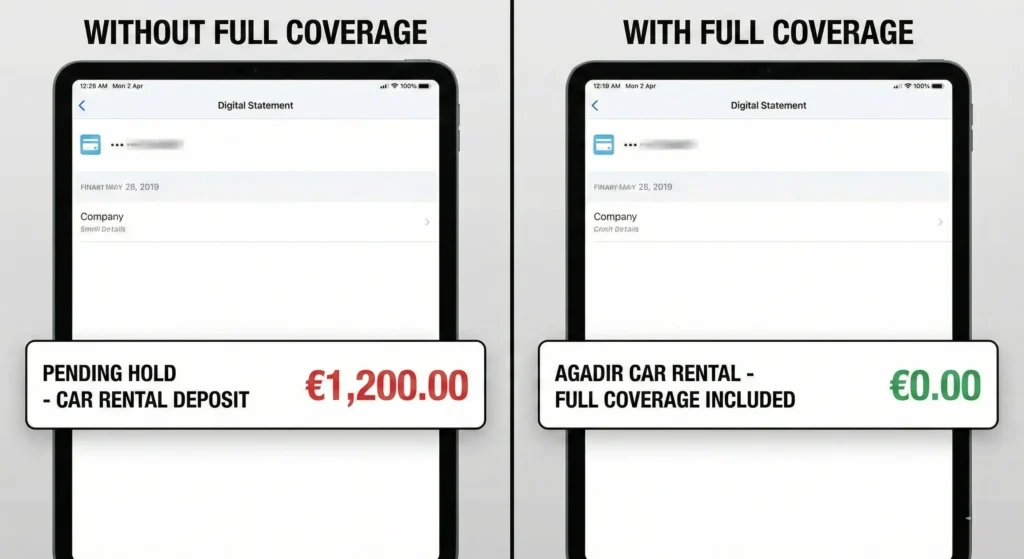

Our All-Inclusive Insurance Model

We build full coverage into our base rate because we got tired of the insurance upsell game. When we quote 23 euros per day, that includes comprehensive CDW and Theft Protection with reduced excess built in. You're not buying "basic" coverage and then getting pitched upgrades at pickup.

Our excess amount varies by vehicle (800-1200 euros depending on the car category), and we're transparent about it in your booking confirmation. More importantly, we don't require deposits for most rentals, which eliminates the credit card hold issue entirely.

This model costs us slightly more in insurance premiums, but it simplifies everything for travelers. You know your total cost upfront. You're not making insurance decisions under pressure at the airport. Your credit card doesn't get tied up with a massive hold.

The exclusions still exist (tires, undercarriage, interior, keys), but we handle damage claims fairly and document everything with photos at pickup so there's no ambiguity about what's new damage versus pre-existing.

Making the Right Insurance Decision

If you're booking with a traditional rental company at Agadir airport, here's how to think about Super CDW:

Buy Super CDW if: You're uncomfortable with 1,000+ euros held on your credit card, you're driving extensively in rural or mountain areas, you're not confident about navigating Moroccan road conditions, or you simply want maximum peace of mind.

Skip Super CDW if: You have third-party annual coverage and don't mind potential claims hassle, you're an experienced driver comfortable with the base deductible risk, or you're only driving minimal distances on main highways.

Consider our all-inclusive model if: You want everything settled upfront with no deposit holds, you prefer transparent pricing over base-rate-plus-add-ons, or you're comparing total costs rather than just advertised daily rates.

The worst approach is ignoring insurance entirely and hoping nothing goes wrong. Morocco's roads mix modern highways with challenging rural routes. Police checkpoints are common, and you need proof of proper coverage. The small savings from skipping insurance aren't worth the potential financial disaster if something happens.

Frequently Asked Questions

Is car insurance mandatory for rentals in Morocco?

Yes. Moroccan law requires all vehicles to carry insurance. Every rental includes basic CDW and Theft Protection by law. The question is whether you reduce your deductible with Super CDW.

What happens if I damage the car without Super CDW?

You pay the repair costs up to your deductible amount (typically 1,000-3,000 euros depending on vehicle). The rental company charges this from the deposit held on your credit card.

Can I use my personal car insurance or credit card coverage?

Personal insurance rarely covers rentals in Morocco. Some premium credit cards offer rental coverage, but verify it's valid in Morocco and covers the full deductible amount before relying on it.

How long does it take for deposits to be released?

Typically 7-14 days after you return the vehicle undamaged. If there's any dispute about damage, it can take longer while the claim is investigated.

Does full coverage mean zero responsibility for any damage?

No. Even Super CDW excludes certain damages like tires, undercarriage, interior, and lost keys. Always check the specific exclusions in your rental agreement.

What should I do if an accident happens?

Stop immediately, call the police for an official report (required for insurance claims), take photos of all damage, contact your rental company's emergency number, and don't move the vehicle until authorities arrive.

How can I avoid disputes about pre-existing damage?

Take comprehensive photos and videos of the entire vehicle (exterior, interior, undercarriage if visible) at pickup with a rental agent present. Do the same at return. Timestamp matters.

The Bottom Line on Rental Insurance

Insurance confusion is by design in the traditional rental model. Companies advertise low base rates, then recover margins through insurance upsells at the desk. The traveler standing there after a flight, tired and uncertain, often just says yes to whatever's recommended.

Our approach eliminates that entire stressful interaction. Comprehensive coverage is included. The price you see is the price you pay. You're protected from the major financial risks without deposit holds or surprise costs.

Whether you choose us or another provider, understand exactly what coverage you're getting, what the deductible/excess amount is, what exclusions apply, and whether deposits are required. Those four factors determine your real insurance protection and total cost.